#8 On regulatory heat, burning ETH and NFT summer

Regulators in the US have been on fire lately. So were NFTs...and especially ETH. Let us brag a little about Deflationary Blocks, our analytics tool for burned ETH

Welcome to issue #8 of Carbono Insights. We are Carbono, and advisory firm specialized in cryptocurrency, and managers of the fund Abacus Carbono. With Carbono Insights we wish to help people get acquainted or up to date with crypto and its many possible approaches.

We would love to hear your comments. Write us at team@carbono.com or find us on Twitter: we are @carbono_com, @raulmarcosl and @mrubio

US Infrastructure Bill

In an unexpected turn of events, the crypto world has been immersed in political activism and lobbying after a legal battle broke out in the US. Of course, everybody knew regulation was bound to happen, but how it showed up has taken the industry by surprise.

It all started in late July. The Biden administration presented the draft for a bipartisan bill containing a plan for activating the American economy through a $1T (one trillion dollars) investment in updating the roads, highways, and digital infrastructure. The government expected some of the funds for the bill to come from taxing the under-regulated area of crypto. In their initial draft, regulators announced a projected income of $25B coming from tax compliance in the crypto sphere. According to the draft, “any person who (for consideration) is responsible for regularly providing any service effectuating transfers of digital assets” would be required to file tax information reports similar to those for securities brokers. The breadth and ambiguity of the definition of broker made the bill unworkable

.

The draft revealed the lack of understanding of crypto coming from the halls of Washington. The superficial choice of words failed to capture the complexity of an industry that is redefining the way we understand companies, corporations, stakeholders, and employer/employee relations... The regulation of the innovative tour de force that is crypto was defined in an annex's fine print. The reaction was swift; the crypto industry fought back.

It was never a matter of money. Many outstanding figures were quick to point out that regulation was expected and desired by the industry too. The word "broker" was the main source of disagreement.

“The broad, confusing language leaves open a door for almost any entity within the cryptocurrency ecosystem to be considered a “broker”—including software developers and cryptocurrency startups that aren’t custodying or controlling assets on behalf of their users. It could even potentially implicate miners, those who confirm and verify blockchain transactions. The mandate to collect names, addresses, and transactions of customers means almost every company even tangentially related to cryptocurrency may suddenly be forced to surveil their users.” The Cryptocurrency Surveillance Provision Buried in the Infrastructure Bill is a Disaster for Digital Privacy.

This degree of surveillance over the industry was perceived as an invitation to flee. The American crypto ecosystem pointed out that this bill could severely impair the country's opportunity to adopt, let alone lead, this historic innovation.

According to the definition of the word broker, software developers, crypto miners, node operators, and other stakeholders were considered brokers and were commanded with the surveillance and reporting of the activity of users. A task so far away from their usual activity that they would have to go out of their way to develop new mechanisms to invade user privacy, defying the basic ethos of crypto.

Expressed in memes, the language of the internet:

Some Senators joined forces with the crypto industry. Ron Wyden, Pat Toomey, and Cynthia Lummis proposed an amendment that pleased crypto. It suggested defining with precision which actors would be considered brokers. . But then, a wild trio of opposing Senators appeared. Rob Portman, Kyrsten Sinema, and Mark Warner produced an alternative amendment that only exempted proof-of-work miners from the reporting requirements. A slight improvement over the original draft, but much worse than Wyden, Tommey, and Cynthia's suggestion. Nevertheless, this proposal was unofficially endorsed by the White House in a position that some have understood as a first attempt to put a leash around DeFi.

The thriller is still unfolding. In its last episode, the second amendment has been the one to move forward, to the disappointment of the crypto community.

There's still hope, and there will definitely be more chapters following the convoluted lifecycle of a bill. The whole process was narrated beautifully from the inside by some insiders like Jerry Brito, Jake Chervinsky, or Kristin Smith, who acted as lobbyists for the industry's interests.

But the most relevant conclusions of this incident are to be extracted from the bigger picture. The infrastructure bill was a call to arms to the crypto industry, and the response surprised everyone. And we mean everyone. Crypto insiders watched with amazement and excitement how an industry that has lived in the margins of mainstream society was able to monopolize the debate around a $1T infrastructure bill sponsored by the president of the USA. This was not just a bunch of nerds and outlaws screaming, "leave us alone!". This was the coordinated response of a trillion-dollar innovative industry fueled by a solid, shared culture. Crypto mobilized quickly, massively, and stayed on message.

It makes sense. We're talking about millions of people who communicate globally and in real-time through Twitter, Telegram, Discord... and work in an environment whose focus is to achieve consensus through common interest and to design incentives thoroughly and transparently.

Crypto is something else. Inherited terms like broker do not easily define it. It does not fit seamlessly in traditional structures, like party politics or borders. The worst possible outcome envisioned by American crypto entrepreneurs was never the possibility of watching the industry die but to imagine it flourishing somewhere else and having to decide whether to choose between their passion or their country.

And one last, but very relevant, "by the way": the market did not react all of this time. Bitcoin, Ethereum, NFTs, DeFi, stablecoins...they all went on with their lives.

⬡ Six Angles

We select six topics to illustrate the very different angles crypto can be approached from. We could choose dozens, but six is the atomic number of carbon… and otherwise we'd be writing for ages.

1. ETHEREUM | DEFLATIONARY BLOCKS

EIP-1559 finally went live on August 5th. For those who need an explanation, but don't have time to read a whole, magnificent post about it, here's a tweet-sized refresher.

Ok, almost tweet-sized. But to be fair, EIP-1559 is quite a complex matter. We are talking about an update that is bringing deflationary features to Ethereum. Since August 5th, every new block is burning ETH. Every transaction, from Mary, sending ETH to John, to Uniswap settling massive coin exchanges to Axies changing hands, triggers the destruction of ETH. Sometimes more, sometimes less. Sometimes so much that there is more ETH burned in a block than ETH generated through block rewards. Every time this happens, the total supply of ETH shrinks a little bit, making every single remaining ETH slightly more valuable.

At Carbono, we wanted to understand the implications a little better. EIP-1559 created a new category of blocks: deflationary blocks. Those where the amount of ETH burnt is higher than the block reward of 2ETH, and therefore reduce the supply of ETH. We were left wondering what the rate of deflationary blocks looked like. How many have happened already? At what pace? Is that pace increasing? What blocks are burning more ETH?

Carbono's own Al went a little crazy and built a site in carbono.com/deflationary-blocks, and now we can see the evolution of things in real-time

We've been able to learn, for example, that so far, around 2% of the blocks mined are deflationary, and the amount of ETH burnt is 30% of the ETH mined.

This means that, in the end, we can consider that the block reward has dropped from 2ETH to 1.3ETH

The maximum fee burnt in one block was 49.74ETH (over $150k), in the middle of an NFT minting spree.

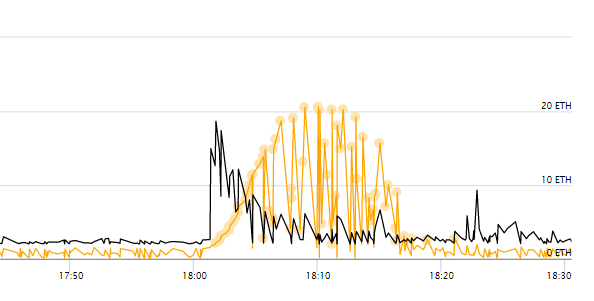

And we have been able to see what the improved UX EIP-1559 looks like. Since the hard fork, the base fee changes in less abrupt, more predictable ways. You can see the curve it creates in the middle of an activity increase (black lines are the 2ETH block reward + miner tips; the orange line is the burnt base fee)

2. REGULATION | SECURITIES EXCHANGE COMMISSION

Regulation also approached crypto from a more predictable angle. In the latest weeks, the chairman of the SEC, Gary Gensler, has been actively expressing his intention to make cryptocurrencies a safe market for all types of investors.

Right now, we just don’t have enough investor protection in crypto. Frankly, at this time, it’s more like the Wild West. Remarks Before the Aspen Security Forum

This is both a bull and a bear sign: regulation is desired by the industry that expects more and more people to approach and benefit from the clarity and security it provides. But regulation also needs to operate with precision if it wants to preserve the pace of innovation.

According to reports, Gensler has several areas of crypto on his radar.

These include matters concerning token offerings, decentralized finance (DeFi) and stablecoins. Other focus points for Gensler’s SEC are custody, exchange-traded funds (ETF) and lending platforms.SEC Chair wants robust crypto regulatory regime for the US

The SEC's activity can be felt in recent events, like the pressure on Binance or the recent fine to Poloniex. Gensler's position seems to be consistent with his employers'. Through its Secretary of Treasury, Janet Yellen, the Biden administration is becoming increasingly vocal against the lack of control over the industry. Regulation is coming.

3. SECURITY | POLY NETWORK'S RECORD-BREAKING HACK

Do you want to know how fast things move in crypto?

On Tuesday, the largest DeFi hack to date took place. The victim was Poly Network, a not very well-known multi-chain decentralized exchange that made this desperate announcement on Twitter, admitting the hack.

We soon learned the hacker had lifted more than $600M. News spread like wildfire on Twitter. According to REKT news, we were witnessing the gold medalist of DeFi hacks, making a 10x on the next in line.

By Wednesday, the hacker had already given back half of the loot. By Thursday, more than half. On Friday, the hacker had reportedly given back most of the stolen money, and he had rejected a $500K tip.

During the time in the middle, Twitter was on fire. Before the first token was retrieved, there we could already access:

In-depth post mortem analyses (I, II,...) revealing the mistakes that allowed the hack to happen. TL;DR, multi-chain technology is very complicated, plus Poly made poor decisions. The hacker exploited "a vulnerability between contract calls."

The interpretations from opinion leaders, like Binance's CEO or investors, explaining what this hack says about the overall sector. TL;DR, Nascent areas, like multi-chain DeFi, still need time to mature. Crypto elders are not surprised by exploits; neither are institutional investors, who are wary of approaching the fringes of DeFi.

The report of a blockchain security firm that claimed to have tracked down the attacker, including email address, IP information, and device fingerprint.

A self-interview by the perpetrator written in the comment block of a transaction. Genius. TL;DR, he did it for fun. He will give everything back.

Security and regulations have been mentioned in the past as the main hurdles for institutional investors to enter the space. This hack and the subsequent PR are probably bad omens for those not interested in scratching more than the surface. But for those willing to read between the lines, this is a story of trailblazers facing challenges (Poly Network's multi-chain solutions inhabit the frontline of DeFi) and a community behaving in ways never seen before. How many cases have you seen of thieves giving back half a billion-dollar loots while his thoughts and methods are cheerfully shared on Twitter?

4. HUMAN RESOURCES | CRYPTO'S HIRING SPREE

In the world of on-chain metrics, big investment, and bigger data, there are some reliable signals of the course of the industry that are more qualitative. Hiring is one of them.

One of the consequences of the recent flood of venture capital into the crypto sphere has been an inflow of talent. Native crypto companies are hiring by the hundreds, especially in the short-supplied market of developers. Not to mention the recruiting spree caused by the ghost of regulation yet to come, which is funneling professionals from the legal and political sphere.

But now, hiring is also happening outside the boundaries of crypto-first companies. We recently saw how the mere listing of a job position for a blockchain expert at Amazon triggered rumors with enormous financial implications. Other financial companies, like PayPal or JPMorgan, are also adding experts to their payrolls, like sailors loading their ships with the necessary gear for a long journey.

5. NFT | SUMMER SEASON

You might remember July was a golden month for NFTs. OpenSea reached record revenues. At the same time, they announced an investment round led by Andreessen Horowitz that turned them into a unicorn. Axie Infinity was the flavor of the month. It had managed to keep growing despite the downward inertia coming from Bitcoin and proved excellent health in all possible KPIs, from players to transactions, to revenue.

Well, August is showing no sign of slowing down.

It was the month for the resurrection of Cryptopunks. The creatures from Larvalabs are, by the time of this writing, reaching $180M in sales in August, already above the $135M of July. In one single week, some notorious punk sales, including one from marketing superstar Gary Vaynerchuck made the news and pushed the sales from adjacent NFT projects.

It's been the month of Kutcher and Kunis's (eventful) launch of Stoner Cats, an animated series where users need to purchase an NFT if they want to watch.

The general optimism dragged classic projects like Bored Apes Yacht Club, a hybrid between avatar and metaverse NFTs, or Art Blocks, the home of generative art NFTs.

NFT is a unique category of assets. It has shown certain independence from the evolution of other investment trends. It is closer to retail investment and private consumption, less liquid, less reliant on hard math, more prone to fads...We are clearly in the middle of NFT summer, with sales booming among the crypto community, especially in its form as collectibles (Cryptopunks, Meebits, Penguins…), although the current pace of new launches seems unsustainable in the long run.

6. ON-CHAIN METRICS | SUPPLY SHOCK

One of the predictors of the price bounce we recently witnessed was the supply shock signs visible in on-chain metrics. A supply shock is the sudden change of supply in an asset that leads to a change in price.

Crypto has its own ways of attempting to predict the way assets will move by analyzing blockchain data. Three examples of signals (credits to Willy Woo) that are a proxy to the intent of investors are:

Exchange supply. The movement of funds between self-custody solutions and exchanges indicates an intention to withdraw or lock assets, resulting in a reduced supply.

Liquidity supply. Investors (or at least their addresses) can be classified as long-term or speculative based on their history of buying and selling. Thus, assets in hodlers' hands are less likely to be available for purchase.

Long Term Holder supply. A similar metric but approached from a different angle. Coins that haven't moved in a long time are unlikely to become liquid.

These and other metrics are the way of quantifying, and therefore attempting to predict investor behavior.

If you enjoyed this issue, don’t forget to share. Carbono Insights is also available in Spanish. Share your thoughts and comments with Carbono at team@carbono.com, or through Twitter: @carbono_com, @raulmarcosl and @mrubio