#71 Ripple's ripples

Ripple achieves a significant win against the SEC, crypto sees record inflows...but prices remain boring.

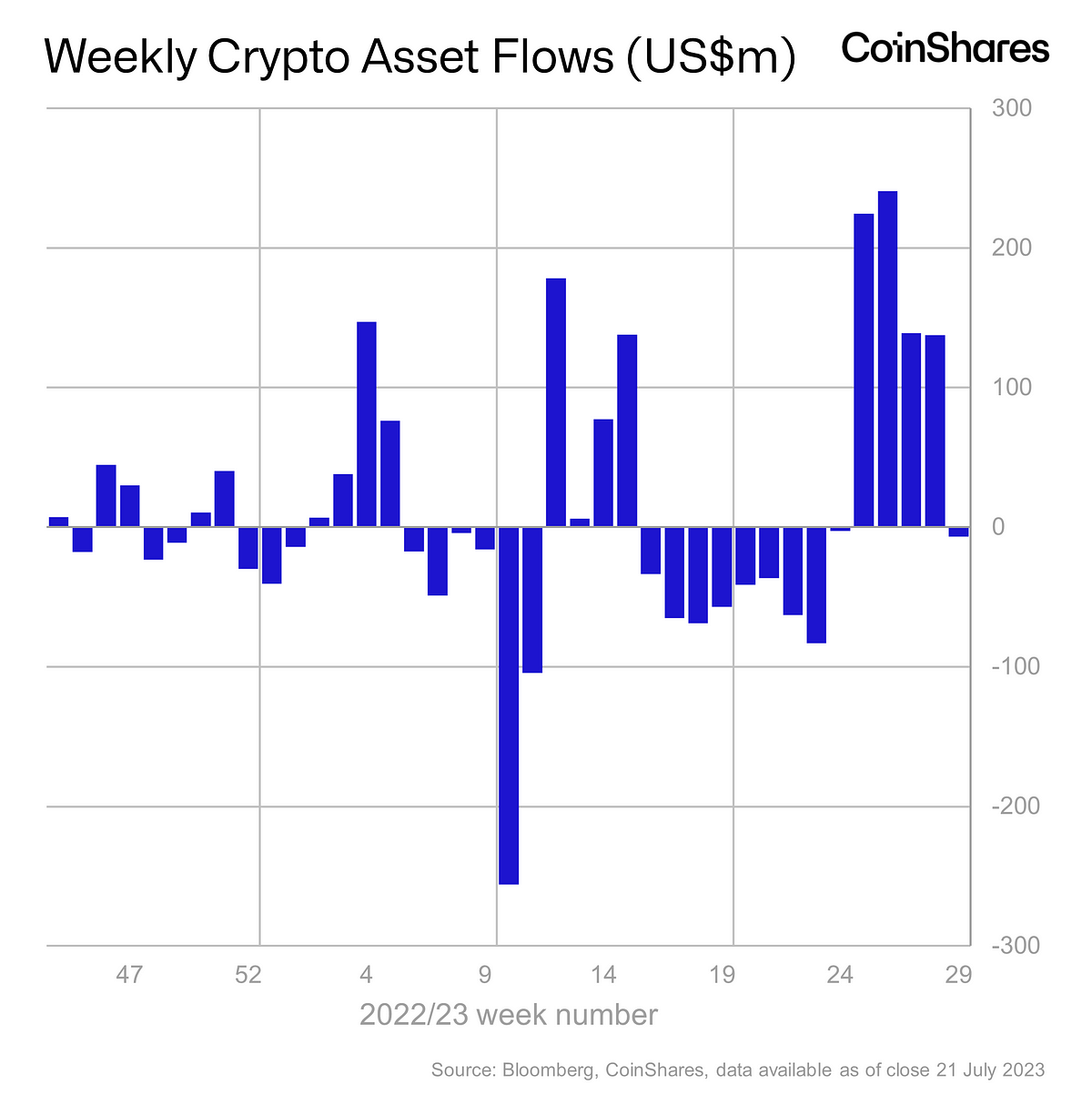

Ripple emerged victorious in its recent battle against the SEC (though the war is far from over), while crypto's inflows reached new heights, as reported by Coinshares. But amidst this excitement, the rollercoaster ride of bitcoin and ether prices has gone remarkably flat, stubbornly resisting the $30k and $2k thresholds. Is it the summer slumber, the looming regulatory uncertainty from the US Senate, or perhaps signals of turmoil in the Chinese economy?

The SEC filed a lawsuit against Ripple in 2020, alleging that the company conducted an unregistered securities offering by selling XRP tokens. For 3 years, crypto has been waiting for a verdict that would indirectly spell out the difference between securities and commodities in crypto. The resolution comes at a time of general good spirits in crypto.

1. Regulation | XRP is and isn’t a security

Ripple scored a victory for crypto with the verdict on its long-standing case. The judge determined that some parts of the sale of XRP cannot be considered a security.

XRP was launched through two avenues: private agreements with institutional investors and a secondary sale in public markets. The private agreement between Ripple and institutional investors has been considered a security because it fits the Howey Test's definition of an expectation of returns from a third party's work. But when XRP was bought freely on secondary markets, the judge assumed that the explicit expectation of returns was not there.

It seems like a win in general for crypto. Many tokens that were threatened by the SEC now have some precedent to hold on to (MATIC, ATOM…). However, the victory cannot be considered final. The SEC can still appeal the decision, and many believe that they have good reasons to turn it around. At the end of the day, what the judge has ruled is that XRP was both a security and not a security, depending on the way it was transferred on the market, which goes against prior securities laws (the law doesn't care about processes, just defines assets). Plus, from a general perspective, the fact that institutional investors agreeing with Ripple need to comply with securities laws, but retail buyers on DeFi don't, seems to go against the spirit of the law. The SEC is supposed to defend unqualified investors, not the other way around.

Gary Gensler has already said this is not over.

2. Interoperability | Chainlink wants to connect TradFi and DeFi

Chainlink, the data oracle company, has launched its Cross-Chain Interoperability Protocol (CCIP) on its mainnet. CCIP creates a standard communication system between different chains. According to Chainlink, CCIP is to blockchains what TCP-IP is to the internet. CCIP currently supports Avalanche, Ethereum, Optimism, and Polygon and has onboarded Aave and Synthetix protocols. CCIP has the potential to connect permissioned and permissionless blockchains, thus creating a bridge between banking use of blockchains and public DeFi.

3. L2s | Rollups on the roll

Where to start? There's so much going on in the L2 space that it's hard to explain it without either explaining things properly or leaving things out.

Polygon is going through a full-blown revolution, with changes in technology, branding, tokenomics, and governance. The latest news is that the $MATIC token is going to be substituted by $POL, the one token to rule them all, as the lifeblood of the wider Polygon ecosystem emerging from the Polygon 2 vision.

In the race between Arbitrum and Optimism, the latter is winning in buzz lately. The most outstanding news is the upcoming launch of Base, Coinbase's OP Stack-based L2.

Consensys is the firm behind Metamask, one of the household names in crypto. Metamask is probably the most popular wallet worldwide. Now Consensys is launching its own zero-knowledge rollup, Linea. Will it become the most popular rollup worldwide?

Starknet, one of the oldest zero-knowledge solutions out there, just launched its development stack for third parties to deploy their own L2s. What's interesting about this is that they are the last in a long line: Optimism, Arbitrum, Polygon… virtually every L2 has launched a dev framework, so it must be a no-brainer. Everyone seems to think that L2s are going to be networks of chains.

4. UX | Telegram bots

Telegram was already one of the most popular tools for crypto users and projects because of its features and privacy-preserving approach. These days it's also becoming a trading tool as many Telegram bots have emerged as the interface for on-chain tasks such as token purchase and exchange, limit orders, copy trading, or wallet analytics.

This taps into crypto's needs for a more convenient interface for DeFi. But their success is also linked to the fact that bots are launched together with a token that accrues value as users pay fees for the operations performed through them.

5. Custory | Nasdaq has left the room.

The word on the street says that Gary Gensler is executing Janet Yellen's anti-crypto quest. But besides grandstanding declarations and lawsuits, most of this battle is taking place through trench warfare that weaponizes the fine print of banking supervision. In this thread, Matt Walsh explains a little trick that the SEC is using to hinder crypto.

The SEC periodically issues notifications called Staff Accounting Bulletins, which establish accounting and reporting requirements for supervised companies. According to SAB 121, published in March 2022, companies offering crypto custody must treat the custodied assets as if their own. This means that a bank that wants to offer custody must include the custodied assets as a liability, and therefore, it must allocate a portion of its capital as collateral. In simpler terms, if Alice deposits 1 BTC in a custodian bank, the bank has to put a proportional amount in USD from its own pocket.

These are the tricks that are preventing professional institutional solutions for crypto asset custody. The latest example is Nasdaq, which announced in September 2022 that it was launching a custody service but has just announced that it is backing out.

6. Report | Q2 2023 Ecosystem Highlights

Overall, we have seen a very positive first half of the year for crypto, with some hiccups along the way due to regulatory pressure from US institutions.

Bitcoin and Ether have surged 83% and 60% year to date. Bitcoin rose 71% in Q1 and 7% in Q2, while Ether rose 51% in Q1 and 6% in Q2. The increase from early 2023 has a lot to do with the fact that crypto was rising from the ashes of the catastrophic end of 2022. Throughout the majority of the second quarter of 2023, though, crypto prices remained relatively stable to downward, with BTC experiencing drops of -1.4% in April and -4.5% in May. However, in June, there was a significant final hike of 14% following the news of BlackRock's BTC spot ETF filing.

You can read the introductory summary included in Abacus Carbono's Ecosystem Highlights report distributed to investors quarterly in our Medium post or download the full report here.