#43 Binance's finances

Will Binance be the next one to fall? It's unlikely, but we can sure extract some lessons from the situation. Also, news from Sushi, we have a date for ETH un-staking and more from FTX.

Welcome to the last Carbono Insights of 2022. This was the first full year of our biweekly newsletter, and what a year. 2022 will be remembered for the chain of debacles, for Terra to FTX, but also from the technical breakthroughs like The Merge that will shape the future of crypto.

Stay with us for another year of Insights.

Binance’s finances

I don’t think people really thought things were that bad chez FTX when Sam was calming down the masses with his (since deleted) tweet saying, “FTX is fine. Assets are fine”. So now that Binance is suffering from a wave of FUD, it’s hard not to give it a quiet thought.

Binance and its founder, Changpeng Zhao, have inherited Sam Bankman-Fried’s / FTX’s throne in terms of visibility. Binance is the #1 exchange in trading volume, and if there were people who hadn’t heard about them from their in-law cryptobro at a Christmas dinner, they’ve probably heard about them now in the news after the most recent events surrounding the FTX meltdown.

A recent perfect storm of setbacks has increased the attention on Binance. Some say they are in trouble and likely to become the next FTX (or, in other words, crypto’s “next-est” Lehman Brothers moment). But how bad are things?

Chronologically, rumors kicked off when the Department of Justice resurfaced a 2018 AML compliance lawsuit. It refreshed investors’ memories and reminded them that Binance was once in the crosshairs of law enforcement for its lax take on regulation. But, like Blockworks, newsletooor Byron Gilliam points out, regulation can be like a dormant volcano. It might look safe, but will it be safe forever?

Some relevant firms such as Jump Capital and Wintermute reportedly removed hundreds of millions from Binance in the same days (unlikely that it’s because of compliance concerns, but who knows), and what happened next will not surprise you: billions followed, beginning a panic bank run.

CZ had quickly published Binance’s Proof of Reserves (reportedly holding over $60B in assets) in response to the FTX debacle, purportedly proving Binance holds enough assets. But what does “enough” mean if you don’t disclose liabilities?

Others criticized some more flaws in Binance’s efforts, like a familiar inability to clearly state their corporate structure and some decision-making and auditing processes. Binance rhymes with FTX: they have a combination of US-regulated and offshore structures with nebulous relations.

Further along the week, the firm that had reportedly audited Binance’s accounts, Mazars, started acting dodgy. They erased all of Binance’s Proof of Reserves records from their website and claimed they would no longer provide those services.

In the meantime, the ghost of SBF refuses to disappear. Binance was one of FTX’s first investors. Somewhere along the road, either CZ wanted out, or SBF wanted to push CZ, but in any case, FTX bought back Binance’s participation in FTX by paying back $2.1B in BNB, BUSD, and the defunct FTT. But the bankruptcy process could consider that transfer illicit and creditors could ask for this money back. And they probably won’t accept crypto, at least not FTT.

So there’s the run on the bank, the shady accounting, the confusing corporate structure, the looming legal risks, and the ghost of FTX's past.

Nothing in this story proves that Binance is genuinely on its deathbed. On the contrary, the facts say that the exchange could sustain a + $ 6B withdrawal fever, and it could hold an even bigger wave.

At the moment, it looks like Binance funds are indeed Safu, and CZ is telling a reasonable amount of the truth. But fortunately, for crypto, “a reasonable amount of truth” is not enough anymore. The best possible outcome would be to see Binance make significant moves towards better accountability and a more transparent and compliant structure and set a higher standard of professionalism in the space.

These bears watching fireworks are our way of saying goodbye to a year worth learning from. Check out our collection of NFTs on Opensea, INTERPOLATIONS OF CARBONO INSIGHTS, and follow our step-by-step intro to purchasing your first NFT if you want to dip your toes in crypto.

⬡ Six Angles

We select six topics to illustrate the different angles from which crypto can be approached. We could choose dozens, but six is the atomic number of carbon… and otherwise, we’d be writing for ages.

1. Decentralized Exchanges | Sushiswap looks for a business model

Sushi’s “head chef,” Jared Grey, recently took to Twitter to shed some light on Sushi’s financials before dropping a significant proposal.

According to his math, Sushi has 18 months of runway based on its current holdings (after slashing operating costs from +$7M to $5.2M), and it has lost $30M in the last 12 months in emission-based liquidity incentives. The conclusion is that Sushiswap needs a new source of revenue from a more sustainable business model.

Sushi’s DAO just approved a signal proposal in this direction.

Aside from the details, the most important conclusion is that one of the most important Dexes in the space is looking into a more sustainable business model that slightly steers away from full decentralization to cope with the bear trend. Sign of times.

2. GBTC | Grayscale’s “tender offer”

The SEC stood their ground recently in their decision to reject Grayscale’s conversion of GBTC into a spot bitcoin ETF. The SEC insists that there is a risk of market manipulation in bitcoin trading. GBTC is being forced to look for alternatives since their product currently trades at almost 50% discount over BTC. One option would be a “tender offer”: Grayscale would offer to buy 20% of GBTC shares for a more favorable price than their current value. If GBTC shares were perfectly liquid, they should trade close to a 1:1 ratio with Bitcoin. Currently, GBTC shares are almost 1/2 of bitcoin’s price.

But this would only happen if/once the ETF is rejected, which might not occur for at least half a year.

In the meantime, Grayscale is pocketing monthly fees from investors, which shrinks their incentives to end this legal battle.

Then there’s the Genesis problem: Genesis and Grayscale are both Digital Currency Group subsidiaries. Genesis is allegedly going through extreme hardship, and a potential meltdown could drag its sister companies.

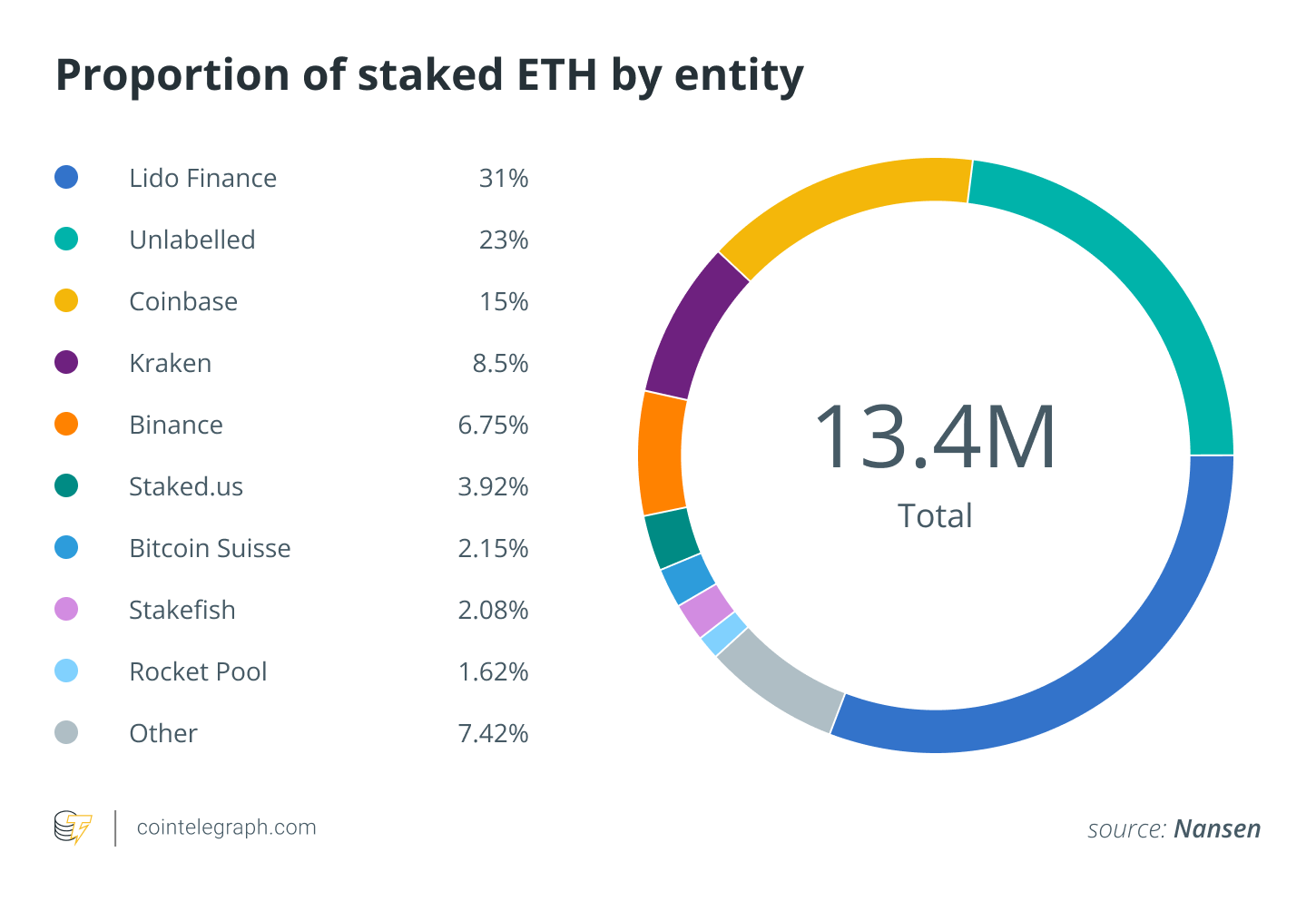

3. Ethereum | A date for un-staking

After eliminating an estimated date for implementing the withdrawal feature in a public roadmap in November, Ethereum developers brought back the un-staking of Ether to the table in their last developer meeting. So now we have a date. By March 2023, the Shanghai fork will have implemented Ethereum withdrawals from the Proof of Stake mechanism, freeing over 15 million ETH (+10% of the total supply) from their shackles.

How much will remain staked is a mystery. Some of the most important staking services (namely Lido, Coinbase, and Rocket) offer liquid staking derivatives that allow investors to benefit from staking rewards while using the staked ETH derivative in DeFi.

4. CeFi | Proof of Solvency

Proof of reserves is a case of self-regulation of the crypto industry. It’s the attempt from centralized crypto companies to offer a similar level of trust to their decentralized counterparties by providing unprecedented levels of transparency and auditability.

But it’s not there yet, and maybe it’s not even enough.

There have been good efforts towards transparency: Binance’s disclosure of their Proof of Reserves after the FTX collapse, Coinmarketcap’s reserve audit feature… Kraken’s Jesse Powell adds two more ingredients for Proof of Reserves to be trustworthy:

Proof of Reserves needs to add Proof of Liabilities to become Proof of Sustainability.

5. Regulation | Warren VS Pantera

Senator Warren, one of the most vocal crypto Palpatines, surfaced a new possible piece of legislation, this time with help from Senator Marshall, from the other side of the political spectrum. TL;DR, once again, politicians are trying to impose “money services businesses” with Know-Your-Customer requirements. In Warren and Marshall's opinion, these “money service businesses” would include miners, validators, wallet service providers, etc.

The US is trying to pass yet another piece of harmful legislation by yielding the argument of bipartisanship and riding the headlines provided by Sam Bankman-Fried. They don’t seem to understand that their proposal will not achieve the desired outcome. Miners, validators, and wallet service providers would have to go far out of their way to implement such measures. So out of their way, it’s more likely that they will either refuse to do it or go bankrupt trying. It’s that or keep out of US soil and citizens, and we’ve seen how that played out with the FTX case.

Let Dan Morehead from Pantera explain why this is a bad idea:

The state of crypto-asset regulation is the polar opposite of the rest of the internet.

The U.S. government literally built the internet (ARPANET which will celebrate the 50th anniversary of TCP/IP next year). The U.S. government then empowered early internet companies with a myriad of Congressional advantages. (…)

So far in the blockchain era, the U.S.’ regulatory approach has had the opposite effect. It has encouraged 95% of blockchain trading to move offshore. Similarly, 95% of the market cap of blockchain protocols are in projects domiciled outside of the United States.

6. FTX | Credible sources

If you like drama, FTX has loads of it. Testimonies from two very credible sources keep confirming the worst suspicions.

John Ray, FTX’s CEO in charge of liquidation, testified before Congress. His version ratified his initial assessment: FTX was a mess. His testimony was filled with headline material. “This is really old-fashioned embezzlement,” Ray said. “This is just taking money from customers and using it for your purpose.” The utter failure of corporate controls at FTX: CEO John Ray III testifies before US Congress

More recently, we also learned that Caroline Ellison and Gary Wang, two of SBF’s closest associates and friends, were engaging in a plea deal with authorities. This wonderful thread summarises their testimony in four words: “It’s what we thought.” Ellison and Wang throw SBF under the bus. They claim that Alameda was managed mainly by SBF, who used it to appropriate customer funds and used it in crappy investments and personal endeavors. It’s in their best interest to point all blame on Sam, but even a lighter version of their testimony confirms some of the worst rumors, like the existence of collusion and special treatment, the deliberate mismanagement of funds (